Case Study provided by Morrison & Foerster

Summary

Morrison & Foerster LLP was a founding member of the California Small Enterprise (CASE) Task Force, which was formed in March 2020 to address the needs of small businesses in California amidst the COVID pandemic. The CASE Task Force (comprised of lawyers, academics, CDFIs, and local business leaders) initially gathered to provide a comprehensive county-level handbook to assist small businesses in navigating the pandemic and also (together with a dozen other law firms) to staff a free, weekly hotline.

The CASE Task Force then also set out to pull together a financing structure to provide recovery loans to small businesses in California, which resulted in the California Rebuilding Fund. The blended finance structure leveraged state guaranty funds (including the California bank guaranty program), philanthropic funds, subordinated loans (from foundations and program related investment (PRI) investors) and senior bank capital to reach underserved small businesses which have been traditionally under-resourced and disproportionately impacted as a result of COVID. The fund used CDFIs to distribute cash, using a coordinated technology platform (run by CRF – another CDFI) and created a new economic model to strengthen and support CDFIs.

The structure is innovative on a number of different levels including: (i) using third party non-profit (Kiva) as the fund manager to allow for donations and PRI investments, (ii) establishing a governance and allocation committee comprised of local leaders, lenders, academics and lawyers to allow for flexible and impartial approvals of changes as the structure progressed, (iii) leveraging government funds and guaranty programs, (iv) bringing loans off balance sheet for CDFIs which is a major limiting factor in their ability to scale and (v) using a technology platform to allow for insight across CDFIs and to ensure fair and equal allocation among all geographies.

1. Beneficiaries

The beneficiaries of the fund are small businesses in California. So far over loans have been made to over 700 small businesses in 36 counties across the state with a total of over $45 million being funded to date. Of the these loans, over 80% have been made to a business owned be a woman or person of color located in a low- or moderate-income community. Indirectly, we are also helping the CDFIs involved in the transaction.

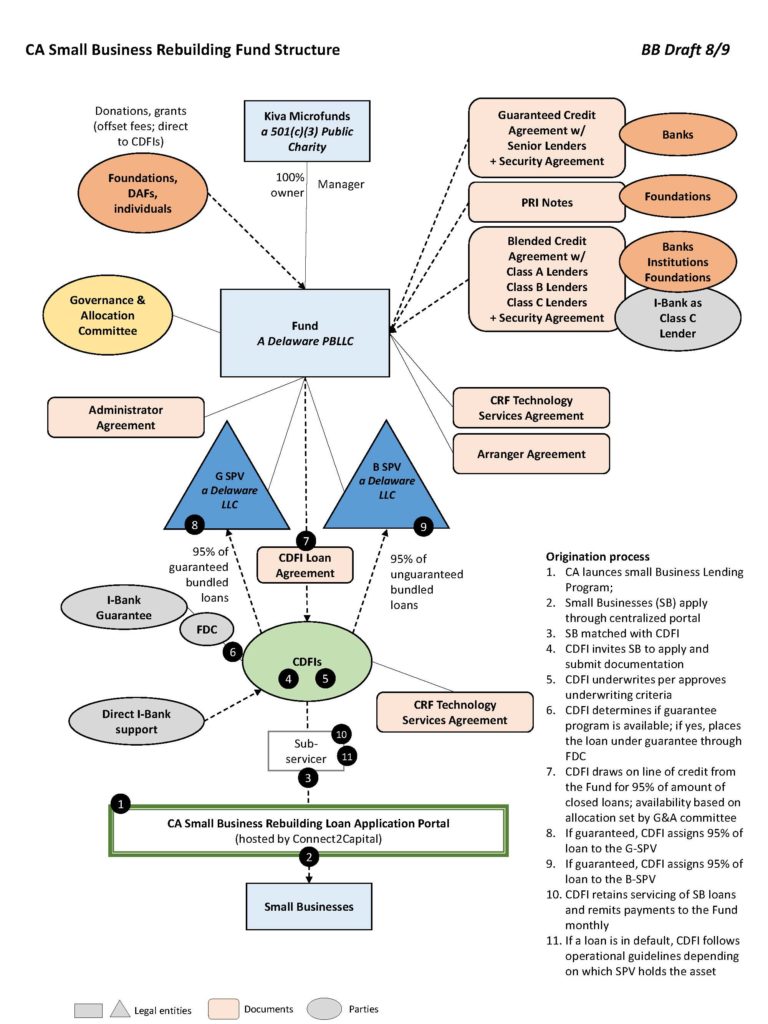

2. Structure

This California Rebuilding Fund structure is innovative on many dimensions:

- It blends government money (either a guaranty of small business loans or providing subordinate first loss guaranty funds into the structure) with donations/grants and PRI capital which forms additional subordinated capital and senior bank capital – this allows us to leverage the subordinated capital to crowd in private capital

- Has a third party owner and management structure which allows for real time changes and decisions to ensure that the mission of the program is achieved – which is helping the smallest of the small businesses which have been most severely affected by the pandemic and left out of other programs such as PPP (ex. the committee is able to ask CDFIs to prioritize certain geographies if we see that small business owners in those areas are falling out of the pipeline)

- Creates a homogenous product so that we can create a pool of assets which we can raise capital for – this is significantly more efficient than each CDFI raising capital on its own

- Creates an off balance sheet structure for the CDFIs – one of the greatest challenges to CDFIs is that they are required to hold significant net assets and as a non-profit growing those net assets is very hard – this structure moves 90-95% of the originated loans off balance sheet for the CDFIs allowing them to do 20x leverage rather than 4x leverage which is typically what they could do

- Uses a single platform for loan applicants – Connect to Capital (CRF’s technology platform) allows for us to see in real time the loans being approved, what loans are not being approved (and the reasons for rejection) and allows us to through the fund structure (committee) to adapt to make sure that we’re reaching the most vulnerable populations (ex. we have found that increasing TA assistance is key to making sure that certain applicants don’t fall out of pipeline), or asking CDFIs to prioritize certain zip codes to ensure equal distribution of funds

- Reducing client acquisition costs for CDFIs – CDFIs have a high client acquisition cost. Coordinating efforts and leveraging Governor Newsom’s communications infrastructure allowed us to get the message out with no cost to the CDFIs. In this structure they did not have to go out to find new borrowers.

- Reaching underserved communities – using the community partners we are able to ensure that we reduce inequalities programs like PPP experienced. They can provide technical assistance and are a trusted resource which encourages under-represented small businesses to apply. These community TA provides (various local chambers) also allowed us to send rejected applicants links to additional resources that could provide assistance even if they did not qualify for a loan through our fund.

Each one of these features requires significant and creative legal thinking and structuring to ensure that they work for all parties involved – and never losing sight of the ultimate mission to provide capital to the smallest of the small businesses with an emphasis on traditionally underserved and under-resourced communities.

3. Impact

The CASE Task Force expect to serve at least 3,000 small businesses with an affordable loan product (4.25% interest with interest only payments for the first 12 months) and hopefully many more as the facility has the ability to upsize to $500 million. We expect to reach due to our intentionality and the partners that we have chosen to work with (CDFIs) businesses and communities which have traditionally been underserved and under-resourced.

In May 2020 Calvert Impact Capital launched the NY Forward Loan Fund. This model was replicated (with modifications) for the California Rebuilding Fund which was launched in November 2020. In early 2021, Calvert also replicated this structure to launch the Southern Opportunity and Resilience (SOAR) Fund which includes 13 states in the South East. Additionally, Governor Inslee has announced state commitment to launch a fund in WA state in spring 2021.

The number of these funds clearly indicates that it can be replicated and each fund contains an accordion feature which allows for it to scale as more capital is committed. The major barrier to scale is finding subordinate capital – state/government funds are key in getting the structure launched quickly. However, the structure does work even without state guaranty (ex. the second CA fund and the SOAR Fund which will have no government money).

4. Goals

The goals of the CASE Task Force is for people, organizations and government to dream big. CASE Task Force would love to see a $10 billion federally funded national program. Initially when we embarked on forming the California Rebuilding Fund, we wanted to launch one or two to prove that this could work and then launch a national program. Unfortunately, since in many circumstances subordinate capital comes from the states, there are geographical restrictions on its use. It is inefficient and costly to create multiple loan funds based upon geography, and our hope is that the Biden administration considers providing loss reserves to support this type of lending. The California Rebuilding Fund and other similar funds have demonstrated that it is effective and easy to scale. A national public-private partnership would enable drastic increases in access to affordable and flexible working capital for small businesses and non-profits owned by women and people of color, those located in LMI communities and who are otherwise un- or under-banked, a population that we think will grow much larger as banks pull back.

5. Case members

The following is a list of participating members of the CASE Task Force:

- Kiva, Calvert Impact Capital, Morrison & Foerster LLP, California Ibank

- CDFIs (CRF, 3Core, Access+Capital, Accion, CDC, ICA, Main Street Launch, Meda, NAAC, Opportunity Fund, PACE, PCV, Working Solutions and others)

- Business support organizations (CA black chamber of commerce, CAMEO, CalAsian, CA Hispanic Chambers, SBDC California, Small Business Majority)

- Lenders and Investors (some have chosen to remain anonymous so this is not a comprehensive list – Wells Fargo, First Republic, Grove Foundation, Kapor, Panta Rhea, All Home, Self Help)

- Other supporters (Berkeley Haas, Berkeley Law, California Governor’s office of business and economic development)

Case Study provided by Morrison & Foerster