This template agreement is provided to you to facilitate due diligence sharing in impact investment.

ImpactTerms has observed that the investment ticket sizes tend to be smaller in impact investing, compared to traditional investments, resulting in the due diligence costs being disproportionately high. As a result, some impact investments may not be pursued due to these high transactional costs. To combat this, many investors are interested in collaborating on due diligence by sharing their due diligence reports, summaries, and due diligence questions.

This can, however, be hampered by the legal risk of being sued by the recipient of the shared due diligence report if the investment subsequently fails.

In light of the above, ImpactTerms has worked with a major international law firm to draft a template agreement to support due diligence sharing for impact investors.

The agreement includes a limitation on the liability of investors that share due diligence material with third party investors, clarification that this sharing of due diligence material does not constitute investment advice and a limitation on any further distribution of the due diligence material.

This template agreement is intended to be used for US investors. This may be used as the basis for an agreement with investors in other relevant jurisdictions, namely the UK and the European Union.

There are more venture capital funds today than ever before, including an encouraging amount that have a focus on social or environmental impact. However, impact investors should be aware of how the very structure and incentives built into venture capital funds can detract from generating impact. Founders often complain of venture capitalists who self-brand as “founder friendly,” while offering little support beyond an investment check.

Being an impact investor is about much more than metrics and measurement. It also includes questioning the structures that govern how we do business, and the power dynamics we sometimes play into.

In a traditional VC transaction, the general partner of a fund invests in a company to provide cash that will help scale the business. Yet, for the founder, such investments often result in ceding control to an investor that prioritizes short term returns over the long-term sustainability and the possibility for purpose-driven business. The founder can feel pressure to dedicate all her energy towards becoming a “unicorn” as soon as possible and maximizing the investors’ profits, rather than focusing on the long-term success of the company. This can commonly include forcing exits for founders, aggressive pressure on founders with little value add, and creating markets where company ownership is uneven and extractive.

What are traditionally considered successful investments from the general partners’ perspective, don’t always translate into successes for the founder or the local market. Imagine a founder left with little equity after years of building a business, simply because the only capital available was venture capital funding. Especially in emerging markets, where most of the investors are based in the U.S. and Europe, the profits generated by successful VC investments are often repatriated, rather than staying in the local market. These extractive measures can result in the company’s mission being overshadowed by the demands of the venture capitalists, and stymies local wealth creation.

Solution

Beyond Capital Ventures is pioneering Equitable Venture, a strategy evolving venture capital by giving founders the opportunity to become co-owners in a fund, and thus align the investor and founder interests. At its essence, Equitable Venture levels the playing field in the power dynamic between the investor and the founders. Beyond Capital recognizes that ultimately, founders work harder than venture capitalists. By offering a stake in the fund’s performance, it is recognizing those efforts.

Founders will receive a profit share in the GP carry based on predefined milestones. By sharing the upside of the fund with the founders, it allows them to become a partial owner in the fund, alongside other portfolio company founders. This concept provides support and incentives from each end of the financial spectrum: immediate capital to grow their business and a long-term stake in what evolves.

Finally, Beyond Capital Ventures is employing Equitable Venture as an incentive to further its focus on gender-smart investing. It will award a bonus of carry points to companies with women on management teams and gender-positive policies.

Implementation

Beyond Capital Ventures has implemented Equitable Ventures by allocating a portion of the GP’s total carry pool to portfolio founders who meet predetermined performance milestones.

The fund will establish a Carry Partnership, or the Carry Pool, as the legal holder of the carried interest generated in the fund, typically a 20% share of the profits generated by the fund, once the limited partners have returned their original investment amount.

Traditionally, the Carry Pool only involves the General Partners, who have been involved in the fund management, and the Venture Partners who have been mainly involved in investment selection.

Beyond Capital will reserve a portion of the Carry Pool, ranging between 5% and 10%, to be allocated to the founders of the portfolio companies invested by the Fund. Portfolio companies that reach the Series A stage of investment will receive an equal share of the Carry Pool. The share is dependent on a series of business and impact metric targets to be assessed over a period of time. Furthermore, company funders will vest over time, so that funders who leave early or on negative terms would not earn their share of the Carry Pool.

Additionally, Beyond Capital Ventures has pioneered the use of a “gender bonus” in equitable venture as an innovative tool to spur reform. Its team wanted to go one step deeper with equitable venture, to have it function as a tool to address gender diversity, one of the fund’s key impact themes. To encourage the investees to promote women into management roles and adopt gender inclusive policies, Beyond Capital is offering an additional bonus to companies that meet certain additional criteria, which include:

Having women being at least 25 percent of all full time employees in the company;

Having at least one woman on the executive management team, or in a senior management position for at least one year prior to the Series A fundraise;

Having at least one woman on the capitalization table;

Gender sensitive policies in place and enforced with regard to all aspects of the business;

Governance structure and mission statement that supports women in the business;

Positive impact of business model on women across the value chain (e.g., suppliers, consumers, etc.).

Companies that meet these criteria will be entitled to a 100 percent bonus of Carry Points relative to companies who do not meet the criteria. These additional criteria will be assessed at the time that the carry points will be allocated.

Replicability – What is Beyond Capital vision around Equitable Ventures and its potential to be replicated and adopted broadly in the impact investing ecosystem?

The goal of Equitable venture is to change the way venture capital behaves in an ecosystem of founders and investors. Beyond Capital views Equitable Venture as a crucial part of a commitment to a holistic, impactful model of investing. It is a seamless structure to integrate, requiring a simple side letter between the General Partner and the founder. Equitable Venture means recognizing the underlying value entrepreneurs create for the fund – and not investing an extractive manner.

Equitable Venture can also supplement an investment strategy. By enabling founders to have a direct stake in our work, you can build an active community of partners who will support each other, and provide high-quality referrals to supplement deal flow.

Finally, Equitable Venture also presents an interesting structural innovation to combat the power dynamics at play. Oftentimes, venture capitalists are the ones who hold all the power. Equitable Venture demonstrates that investors are thinking about the founders. It’s a way to combat the transactional nature of the investor-founder relationships by sharing upside with portfolio companies, as they are the ones working the hardest to generate that upside.

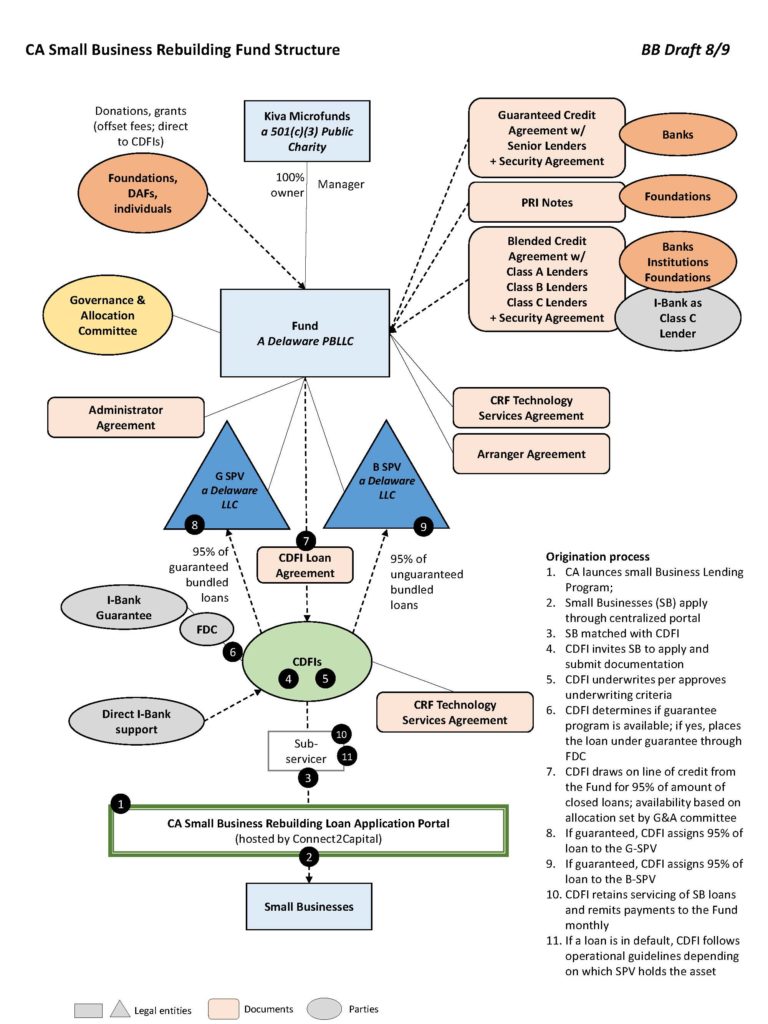

Morrison & Foerster LLP was a founding member of the California Small Enterprise (CASE) Task Force, which was formed in March 2020 to address the needs of small businesses in California amidst the COVID pandemic. The CASE Task Force (comprised of lawyers, academics, CDFIs, and local business leaders) initially gathered to provide a comprehensive county-level handbook to assist small businesses in navigating the pandemic and also (together with a dozen other law firms) to staff a free, weekly hotline.

The CASE Task Force then also set out to pull together a financing structure to provide recovery loans to small businesses in California, which resulted in the California Rebuilding Fund. The blended finance structure leveraged state guaranty funds (including the California bank guaranty program), philanthropic funds, subordinated loans (from foundations and program related investment (PRI) investors) and senior bank capital to reach underserved small businesses which have been traditionally under-resourced and disproportionately impacted as a result of COVID. The fund used CDFIs to distribute cash, using a coordinated technology platform (run by CRF – another CDFI) and created a new economic model to strengthen and support CDFIs.

The structure is innovative on a number of different levels including: (i) using third party non-profit (Kiva) as the fund manager to allow for donations and PRI investments, (ii) establishing a governance and allocation committee comprised of local leaders, lenders, academics and lawyers to allow for flexible and impartial approvals of changes as the structure progressed, (iii) leveraging government funds and guaranty programs, (iv) bringing loans off balance sheet for CDFIs which is a major limiting factor in their ability to scale and (v) using a technology platform to allow for insight across CDFIs and to ensure fair and equal allocation among all geographies.

1. Beneficiaries

The beneficiaries of the fund are small businesses in California. So far over loans have been made to over 700 small businesses in 36 counties across the state with a total of over $45 million being funded to date. Of the these loans, over 80% have been made to a business owned be a woman or person of color located in a low- or moderate-income community. Indirectly, we are also helping the CDFIs involved in the transaction.

2. Structure

This California Rebuilding Fund structure is innovative on many dimensions:

It blends government money (either a guaranty of small business loans or providing subordinate first loss guaranty funds into the structure) with donations/grants and PRI capital which forms additional subordinated capital and senior bank capital – this allows us to leverage the subordinated capital to crowd in private capital

Has a third party owner and management structure which allows for real time changes and decisions to ensure that the mission of the program is achieved – which is helping the smallest of the small businesses which have been most severely affected by the pandemic and left out of other programs such as PPP (ex. the committee is able to ask CDFIs to prioritize certain geographies if we see that small business owners in those areas are falling out of the pipeline)

Creates a homogenous product so that we can create a pool of assets which we can raise capital for – this is significantly more efficient than each CDFI raising capital on its own

Creates an off balance sheet structure for the CDFIs – one of the greatest challenges to CDFIs is that they are required to hold significant net assets and as a non-profit growing those net assets is very hard – this structure moves 90-95% of the originated loans off balance sheet for the CDFIs allowing them to do 20x leverage rather than 4x leverage which is typically what they could do

Uses a single platform for loan applicants – Connect to Capital (CRF’s technology platform) allows for us to see in real time the loans being approved, what loans are not being approved (and the reasons for rejection) and allows us to through the fund structure (committee) to adapt to make sure that we’re reaching the most vulnerable populations (ex. we have found that increasing TA assistance is key to making sure that certain applicants don’t fall out of pipeline), or asking CDFIs to prioritize certain zip codes to ensure equal distribution of funds

Reducing client acquisition costs for CDFIs – CDFIs have a high client acquisition cost. Coordinating efforts and leveraging Governor Newsom’s communications infrastructure allowed us to get the message out with no cost to the CDFIs. In this structure they did not have to go out to find new borrowers.

Reaching underserved communities – using the community partners we are able to ensure that we reduce inequalities programs like PPP experienced. They can provide technical assistance and are a trusted resource which encourages under-represented small businesses to apply. These community TA provides (various local chambers) also allowed us to send rejected applicants links to additional resources that could provide assistance even if they did not qualify for a loan through our fund.

Each one of these features requires significant and creative legal thinking and structuring to ensure that they work for all parties involved – and never losing sight of the ultimate mission to provide capital to the smallest of the small businesses with an emphasis on traditionally underserved and under-resourced communities.

3. Impact

The CASE Task Force expect to serve at least 3,000 small businesses with an affordable loan product (4.25% interest with interest only payments for the first 12 months) and hopefully many more as the facility has the ability to upsize to $500 million. We expect to reach due to our intentionality and the partners that we have chosen to work with (CDFIs) businesses and communities which have traditionally been underserved and under-resourced.

In May 2020 Calvert Impact Capital launched the NY Forward Loan Fund. This model was replicated (with modifications) for the California Rebuilding Fund which was launched in November 2020. In early 2021, Calvert also replicated this structure to launch the Southern Opportunity and Resilience (SOAR) Fund which includes 13 states in the South East. Additionally, Governor Inslee has announced state commitment to launch a fund in WA state in spring 2021.

The number of these funds clearly indicates that it can be replicated and each fund contains an accordion feature which allows for it to scale as more capital is committed. The major barrier to scale is finding subordinate capital – state/government funds are key in getting the structure launched quickly. However, the structure does work even without state guaranty (ex. the second CA fund and the SOAR Fund which will have no government money).

4. Goals

The goals of the CASE Task Force is for people, organizations and government to dream big. CASE Task Force would love to see a $10 billion federally funded national program. Initially when we embarked on forming the California Rebuilding Fund, we wanted to launch one or two to prove that this could work and then launch a national program. Unfortunately, since in many circumstances subordinate capital comes from the states, there are geographical restrictions on its use. It is inefficient and costly to create multiple loan funds based upon geography, and our hope is that the Biden administration considers providing loss reserves to support this type of lending. The California Rebuilding Fund and other similar funds have demonstrated that it is effective and easy to scale. A national public-private partnership would enable drastic increases in access to affordable and flexible working capital for small businesses and non-profits owned by women and people of color, those located in LMI communities and who are otherwise un- or under-banked, a population that we think will grow much larger as banks pull back.

5. Case members

The following is a list of participating members of the CASE Task Force:

Kiva, Calvert Impact Capital, Morrison & Foerster LLP, California Ibank

CDFIs (CRF, 3Core, Access+Capital, Accion, CDC, ICA, Main Street Launch, Meda, NAAC, Opportunity Fund, PACE, PCV, Working Solutions and others)

Business support organizations (CA black chamber of commerce, CAMEO, CalAsian, CA Hispanic Chambers, SBDC California, Small Business Majority)

Lenders and Investors (some have chosen to remain anonymous so this is not a comprehensive list – Wells Fargo, First Republic, Grove Foundation, Kapor, Panta Rhea, All Home, Self Help)

Other supporters (Berkeley Haas, Berkeley Law, California Governor’s office of business and economic development)

In a standard venture capital or private equity fund, the fund manager is entitled to 20% of the fund’s profits. This is known as the “carried interest.”

The innovation of Buckhill Capital and Morrison & Foerster is a set of provisions that can be imported into the relevant documents of most venture capital or private equity fund so that the carried interest is paid out to a fund manager only to the extent that the fund achieves quantified, verifiable impact metrics agreed upon by the fund manager and the fund’s investors. This has the potential to create billions of dollars of incentives for institutional investment managers of all kinds to pursue impact goals alongside financial returns.

Background

Henrik Jones and his company, Buckhill Capital, seek to “finance companies on a mission.” In the course of doing this work, Buckhill encountered a multitude of companies and investment funds claiming to seek environmental, social, and other impact goals, along with delivering a compelling financial return. At times, after investors have signed their agreements and wired their money, Buckhill has observed that the initial focus on impact alongside financial return has faded or took a back seat to financial return and even disappeared altogether. Even when a company or fund addresses impact in the narrative of its periodic reports, it does not always get the same rigorous treatment that the financials get.

Buckhill was not aware of any investment fund manager that has its receipt of carried interest depend directly on whether or not the fund achieves quantified impact goals that are independently audited and verified and that has done so in a manner specifically designed to be easily repeatable and used at scale by other fund managers.

Buckhill decided to things differently when it was presented with an opportunity to gather a group of investors and pitch itself as an attractive source of Series A funding to a highly impactful socially responsible company, Higg Co, that was spinning out of the Sustainable Asset Coalition. Buckhill did not want to give mere lip service to impact and wanted to “put its money where its mouth was” and do something different. That something is the Carried Interest by Verified Impact Calculations (CIVIC).

Carried Interest by Verified Impact Calculations (CIVIC) innovation

BHI’s Carried Interest by Verified Impact Calculations (CIVIC) began with Buckhill’s vision of materially and financially aligning a fund manager’s interests with those of its impact-minded investors and impact-minded portfolio companies. It took the Social Enterprise + Impact Investing team at Morrison & Foerster to fully flesh out and implement the idea both in a way that would work for BHI and its investment into Higg Co but, per Buckhill’s directive, for any venture capital or private equity fund looking to do the same.

CIVIC Overview

The first key feature is the modularity of the BHI CIVIC approach. The documentation Morrison & Foerster prepared for BHI is set up so that any venture capital or private equity fund manager can customize and integrate the CIVIC distribution mechanics from BHI’s term sheet and BHI’s operating agreement into their own fund’s term sheet and operating agreement, leveraging the work that Buckhill and Morrison & Foerster have already done in thinking through some of the details discussed below.

The CIVIC mechanics then reference to a separate quantified Impact Test, which sets forth the quantified impact test for BHI or another fund. The quantified Impact Test is designed to be fully customizable on a fund-by-fund basis. This gives flexibility for different funds to have different impact goals, in different ways, and on different timelines. So the CIVIC provisions do not need to be reinvented with each fund, but each fund has full freedom in defining its own impact goals.

The other key features are reflected by the terms of the CIVIC provisions. To implement BHI’s general idea, Morrison & Foerster thought through some of the details that the solution would need to address. For example, is it more appropriate to the Impact Test be a staged, cumulative test (e.g., whereby the real goal is to reduce carbon emissions by X tons by year 10, but with interim, trend-line goals along the way) or a series of independent annual tests (e.g., prevent X tons of carbon in year 1, then regardless of year 1 results, prevent Y tons of carbon in year 2). Morrison & Foerster advised that the test use the former approach, as it better allows for the potential high variation year to year as a fund pursues impact goals that are intended to be achieved over its entire term. A related issue is what happens if a fund does not meet its interim goal for a given year — does the fund manager forever lose the carried interest associated with that year, or can the fund manager earn it back by overly successful follow-up years that get the fund back to the desired trend-line vis-à-vis its impact goals?

Morrison & Foerster advised allowing the fund manager to earn back carried interest not received in a previous year, again because the impact goals are determined by the desired end of a long journey, and at the outset we might know the rate of progress along the way.

Buckhill hopes that the CIVIC waterfall will be a standard in impact investing and promote accountability of fund managers across the entire ecosystem. By promoting its adoption, if it is not already in fund documents, investors will have the knowledge to ask for the term.

The Capital Access Lab (CAL) is a national pilot initiative that aims to find, promote, and scale innovative investment managers who are providing new kinds of capital to underserved entrepreneurs and communities in the United States.

In July 2020, the Capital Access Lab announced its investments in 5 funds investing in underserved entrepreneurs through innovative investment structures: 1863 Ventures, Anzu Partners, Capacity Capital, Collab Capital, and Indie.vc. During the selection process of these 5 funds, the Capital Access Lab identified over 100 funds focused on underserved entrepreneurs. This report analyzes the approach of a subset of 20 funds that responded to our survey.

Through our analysis, we learned that funds investing in underserved entrepreneurs through alternative investment structures are often nimble investment vehicles that operate in the very early stages of the portfolio companies’ development, really enabling these companies to raise the first essential capital to fuel their growth. They do not invest exclusively in high growth sectors like traditional VCs; our study shows that they are often sector agnostic and have a wide range of return expectations and initial criteria for the investment that are much more flexible than what we typically see in traditional venture capital.

Whereas these funds face challenges related to covering the structural and operational costs of running an investment fund with relatively low Asset Under Management, they represent a nascent and very targeted approach to serving underserved entrepreneurs. Through this report, we hope to highlight their work, support their growth, and inspire potential funders and donors to invest in them.

BACKGROUND

The Toniic Institute, through the Impact Terms Platform, developed this report about the work of the Ewing Marion Kauffman Foundation and the Capital Access Lab on investment funds adopting alternative investment instruments. The Capital Access Lab is designed to provide risk capital to new investment models that do not resemble traditional venture capital or lending, spurring the formation of new financing mechanisms that increase capital investment to underserved entrepreneurs who have been historically left behind due to their race, ethnicity, gender, socioeconomic class, and/or geographic location.

The objective of this report is to review the lessons learned from the Capital Access Lab’s work and to share innovative ways investors can invest in entrepreneurs who are underserved by venture capital and traditional lending structures. Our goal is to describe emerging approaches to investments, liquidity, and risk/return profiles that can be more inclusive for entrepreneurs.

The Capital Access Lab (CAL), formed in 2019, is a national pilot initiative that aims to find, promote, and scale innovative investment managers who are providing new kinds of capital to underserved entrepreneurs and communities in the United States. The Capital Access Lab was created to help address this capital gap by creating a new vehicle to invest in alternative capital funds survive those entrepreneurs That same year, the Lab’s lead investor and sponsor, the Kauffman Foundation, released a report, titled “Access to Capital for Entrepreneurs: Removing Barriers”, which observed that a surprisingly high percentage of entrepreneurs – more than 83% – do not access bank loans or venture capital.

To source prospective funds, the Capital Access Lab created an online application process through which funds or proposed funds could apply for consideration for funding. The CAL did not widely publicize the announcement of this opportunity and instead relied primarily on word of mouth and limited media. When the fund application was announced, responses far exceeded their expectation. CAL had expected 20 to 40 funds to apply in the first year but ended up receiving close to 150 applications. Of those, over 100 fit the requirements for application. “One of the most positive signals to us – [was that] the submissions were mostly first-time fund managers and aspiring investors wanting to bring capital to their community” said John Tyler, Kauffman Foundation General Counsel. The CAL team was also encouraged and surprised by the diversity of the applicants. Roughly 55% of applicants were women and 50% persons of color. The large and diverse application pool reveals a significant demand for and interest in alternative capital structures.

The CAL had expected that many of the applicants would be larger funds that saw alternative capital structures as an additional opportunity. (Traditionally it is difficult for funds smaller than $10 million in assets to generate enough fees to cover their overhead.) Unexpectedly, the applicant pool included many smaller funds that would have traditionally been considered too small to rely only on traditional management fees, but instead many funds were a part of related organizations that could support the overhead. These related organizations included nonprofit business accelerators, Community Development Financial Institutions (CDFIs), and other organizations that wanted to bring investment capital to their communities. For example, 1863 Ventures, one of the funds that received investment, already had an active business development program and wanted to start an investment fund as a means of furthering its mission.

During their due diligence process, the Capital Access Lab identified over 100 funds focused on underserved entrepreneurs, eventually selecting five: 1863 Ventures, Anzu Partners, Capacity Capital, Collab Capital, and Indie.vc.

The Capital Access Lab includes as one of its initiatives, the Capital Access Lab Fund which is a donor advised fund housed at Impact Assets. That fund was capitalized by the Kaufman Foundation. The Capital Access Lab Fund, and a separate funding source from Rockefeller foundation, have invested in the five funds that were selected by The Capital Access Lab.

To ensure the preservation of a recognized charitable purpose under Section 501(c)(3), the Kauffman Foundation developed a charitability term sheet which it has made publicly available as an example of how a foundation structured a particular investment to further its charitable mission and ensure accountability thereto.

Although CAL could not invest in all the funds, they recognized there was a lot to learn and share about their innovative investment structures. This report analyses the approach of a subset of 20 funds who responded to our survey.

RESEARCH – RESULTS AND ANALYSIS

Toniic and the Impact Terms Platform conducted research for this study using a combination of interviews with the principals and a formal survey. The survey participants consist of funds that had applied to the Capital Access Lab during their initial funding period. Twenty funds participated in the survey. The data below highlights some key takeaways from our review.

FUND CHARACTERISTICS

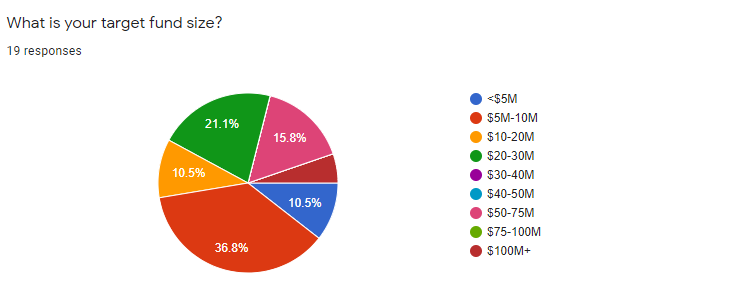

TARGET FUND SIZE

Fifty percent of survey respondents reported a target fund size of less than $10 million.

This target size is consistent with the population of over 100 applicants who applied for funding from CAL – as 50% of those applicants also reported a target size under $10 million. If these funds were to use the traditional VC fee structure that means that they would expect to receive under $200,000 per year in management fees to cover management costs. These low fees are generally considered below the viable amount required by a fund management team without external middle and back office support.

INVESTMENT STAGE

Ninety five percent of participants report that they will invest in seed or pre-seed stage companies. Of those participants, 55% said they would also invest in Series A investments, leaving 45% who only target seed or pre seed stage investing. Only one fund participant would not invest in seed or pre seed stage companies targeting only post seed investments.

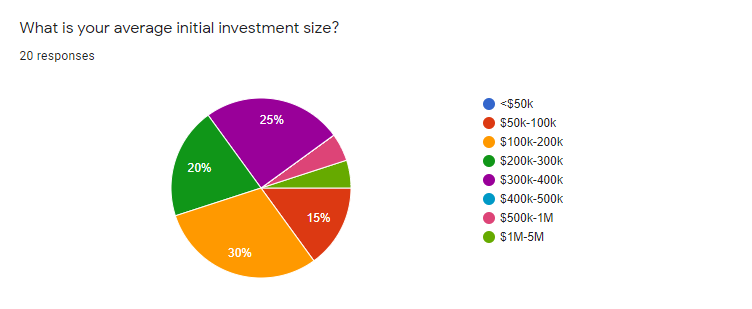

TARGET INVESTMENT SIZE

Consistent with the small average target fund size and largely seed stage investing, 65% of the participants expect to invest less than $300,000 per investment. Only 10% of respondents would invest more than $500,000.

TARGET SECTORS

45% of the respondents have indicated that they are sector agnostic, and 25% of the respondents (among the open-ended responses) included Food and Agriculture as one of their funds’ focus areas.

While traditional VC funds often target high growth sectors such as IT, Health Care, Financials, Telecommunication, the survey respondents did not indicate a strong tendency towards these sectors.

FINANCIAL INSTRUMENTS USED

The following section analyses the financial instruments used by these funds to invest in underserved entrepreneurs. The classification process of these alternative investment structures is a challenging process because there is not an agreed-upon vocabulary for many of the emerging investment structures, nor agreement about whether they should be broadly classified as equity or debt. For example, respondents may have differing opinions about if the Demand Dividend Structure should be debt or equity, so we asked about that structure as both debt and equity then combined them when appropriate to our analysis.

COMMON FEATURES OF ALTERNATIVE INVESTMENT STRUCTURES BASED ON CONTINGENT PAYMENTS

To structure these investments, investors typically start with a target IRR, make a range of estimates of the company’s future performance, and then structure the other terms and features of the investments, including the repayment terms such as the percent of revenues and return multiple cap to achieve that target IRR.

The survey asked a series of questions about the details of the alternative investing structures used by that participant. The questions were designed to get further details around what we anticipated would be the most common structures used: a variation of contingent payment structures. Seventy-five percent of the respondents reported using some form of alternative investment structure based on contingent payments (revenue-based debt, redeemable equity, or Demand Dividends).

These structures are flexible and can be designed to include a variety of features. The core feature of these structures is that they are contingent on something like the amount and timing of the portfolio companies’ revenues. Therefore, the return to the investor will vary based on the features of the investment and the financial performance of the company.

Basis of calculation

Of the 75% participants that stated they will or do use a form of contingent payment structure – 40% said they would invest using gross cash receipts as a basis of calculation, and 47% reported they would invest using net cash receipts. Thirteen percent reported they would use either gross or net cash receipts. Demand Dividend structures did not seem to affect this ratio, even though Demand Dividends typically use net cash receipts as a basis of calculation.

Return Expectations

Respondents reported a wide range of target IRR for their investments ranging from 2% to 35% and averaging 15%. We did not specify if we were asking for the target IRR for the fund or individual investment, but we believe that most participants were answering at the fund level.

Minimum annual revenue required for investment

Respondents reported a wide range of minimum required revenues for the investees ranging from under $50,000 per year to over $5 million per year. The median required revenues was $300,000-$400,000 per year.

Minimum annual revenue growth rate

Respondents reported a median required forecast annual revenue growth of 20-30% with only 16% requiring revenue growth of more than 40%. This differs significantly from the kind of minimum revenue growth requirements you would see from traditional VC.

Half of those who are making revenue based (or similar) finance structures are investing in seed or pre-seed, and will invest into forecast revenue growth below 30%. These characteristics are not common in traditional venture capital so this demonstrates the growth of new sources of capital, that are willing to invest with non-traditional approaches.

Minimum gross margin of target companies

Considering the role that revenues play in the calculation of repayment, we also asked about the minimum required gross margin in order to repay the investment. Respondents reported a minimum median target gross margin of 30-40%. At Impact Terms, our expectation was that lower reported minimum revenue growth rate targets would result in higher the margin requirements. We had this expectation because for an investor to receive a target return of X% on an investment in a lower growth company, that company typically must be able to support a higher percentage of cash flow paid to the investor which requires higher gross margins.

The opposite was the case, as it turned out. The funds that were willing to take the lowest forecast revenue growth in seed stage companies were also willing to take the lowest gross margins. Like the wide range in target IRR, this demonstrates that there is a much wider range of return expectations and minimum requirements than we see in traditional venture capital. One possible explanation is that the funds accepting lower gross margins for lower revenue growth companies are doing so as part of a strategy to provide the appropriate capital to the entrepreneurs. That is, the entrepreneurs they are targeting may simply not have higher revenue growth and margins so the funds used alternative investment structures with return features that the companies could afford.

Percentage of revenue used to repay the investment

Thirty-three percent of respondents indicated that their average percentage of revenues used to repay the investment is 5%, and overall 66.6% indicated an average percentage of revenues lower than 10%. This is typically repaid by the portfolio companies monthly or quarterly out of minimum targeted gross margins of 30-40%.

Average return multiple cap

Thirteen participants use an average return cap – meaning the average cash-on-cash multiple of the invested capital to be returned to the investor over the life of the investment. The industry average return cap is generally between 2x and 3x the initial invested amount. As an example – a cap of 3x on a $100,000 investment would mean the investment is complete when a total of $300,000 has been repaid. This is a common structuring feature of alternative investments that are based on revenue, cash flows or similar contingent payments. The total IRR of that investment would depend on the time it takes for repayment as well as the cap, so a 3x cap investment that takes 10 years to pay out would have a lower IRR than a 3x cap investment that takes 5 years to pay out.

REVIEW AND CONCLUSIONS

It is clear both from the large number of applicants for Capital Access Lab funding and from the follow up research we conducted that there is a significant and underserved ecosystem of small funds that are leveraging alternative investment structures to invest in companies focused on underserved populations. Many of the funds are sector agnostic and not many are targeting traditional venture sectors like IT, Health Care, Financials, Telecommunications. It is also evident from the wide range of return expectations and the combination of investment structuring features that the funds are willing to invest beyond what we would expect from traditional VCs and that therefore that the funds in the survey can serve entrepreneurs who fall outside of traditional VC requirements.

These funds are nimble investment vehicles that operate in the very early stages, potentially being the first professional investors supporting companies in their infancy, effectively de-risking and capitalizing early-stage entrepreneurs.

They also have a wide range of return expectations, including repayment multiples, and initial criteria for the investment that are much more flexible than what we typically see in traditional venture capital. It has long been a complaint that sources of capital are too fixated on structures designed only for companies with explosive growth, so it is encouraging that this research shows an emergence of new capital providers exploring alternatives to traditional expectations and structures.

Out of the 100 funds that applied to the Capital Access Lab, and more specifically out of the 20 survey respondents, we have observed that about 50% of the funds have a target raise of less than $10 million and 75% of less than $30 million; that 95% invest in seed stage, and about ~50% in pre-seed and Series A; and that 65% target an initial investment of less than $300,000 per investment.

Toniic, the global action community for impact investing, has also identified the emergence of relatively small and nimble funds (less than 15M in target AUM) leveraging alternative investment structures to address the needs of underserved populations across different investment themes. These includes funds providing loans to farmers to be repaid through a revenue share agreement in order to allow time to the farmers to switch to organic and regenerative agriculture practices and align their cash flows from higher quality produce with the loan repayment, funds providing capital to minority owned businesses in geographies out of the radar of major venture capitalists to facilitate exits, but also funds providing loans to underserved students that can repay their loans only when they start generating income from actual employment.

While this did not apply to the five funds selected for investment by the Capital Access Lab, these smaller funds are much smaller than typical venture capital fund and CDFI, so small in fact that many are unlikely to cover their operating costs as a fund, and instead use the fund as an addition to existing community service programs. These funds primarily target seed stage companies and are using a wide range of alternative investment structures.

In order to support these experimental but smaller funds, it is clearly important to find ways to lower their operating costs. As noted in this review, important costs like legal, including the added costs associated with using new investing and organization structures, insurance and fund administration are high for these funds. It can even be difficult to find fund administration services that will support alternative investment structures. Companies like AngelList are starting to provide some of these services at lower cost but they are still expensive for small funds and they do not offer services to most alternative investment structures. Investors and foundations who wish to support these funds might consider funding start-ups that help provide these services at lower cost to smaller funds.

Agnes Dasewicz, Lead, Capital Access Lab observed that, alternatively, it would be worth evaluating if investments coming from foundations could, when legally allowed, be accompanied by separate resources and donations to cover some administrative expenses and technical assistance. This is fairly common practice with large international funds who often have sidecar vehicles for technical assistance, and we agree that sidecar grants would help further the ability of small funds to continue to innovate.

John E. Tyler III; General Counsel, Secretary, and Chief Ethics Officer; Ewing Marion Kauffman Foundation

Robert A. Wexler; Principal; Adler & Colvin

Program Related Investments (PRIs) are a tool traditionally associated with private foundations. That is because U.S. federal law imposes specific compliance obligations to regulate private foundation activities. Those laws recognize PRIs as exceptions to some of those obligations. As such, those laws encourage private foundations to use PRIs. While compliance positioning suggests applications limited to private foundations, the use of PRIs is not and should not be so limited. Their use by others can unlock and address opportunities to align market engagement with pursuing and achieving charitable objectives while still preserving and even growing capital.

What are PRIs generally?

Under United States federal tax law, private foundations can presume that grants to organizations exempt from taxation under 501(c)(3), which we generically call “charities,” satisfy compliance obligations under law. That is why most foundations focus so much on grants to charities. Foundations can also make grants to non-charities, including for-profit companies, as long as the foundation exercises what’s called “expenditure responsibility.” Of course, in both instances, grants are money given with no expectation of its preservation, growth, or return – at least in any way that financially benefits the foundation.

PRIs are a tool that the United States Congress has made available to foundations to get money to others while allowing the foundation to have and impose expectations that money can be returned to the foundation and even grown with interest, dividends, and/or capital gains. The foundation can then redeploy those funds again for its charitable purposes.

Among the still too few PRIs that foundations make, most are in the form of loans; some are guarantees. Even fewer are equity investments. All three and derivations of them are allowed.

From a regulatory compliance standpoint, the essential core of PRIs is two-fold. First, the PRI must significantly further the specific private foundation’s charitable purposes under 501(c)(3) and but for that connection, the foundation would not make the PRI. Thus, “charitability” of purpose must dominate for the foundation, although not necessarily for the entire venture or enterprise. The second purpose reinforces the first: no significant purpose for the foundation in making the PRI may be the production of income or appreciation of value. Thus, “owner”-like financial interests may not be significant; not only may they not predominate, they may not be significant, which helps preserve charitability as the priority.

That emphasis on charitability allows private foundations to count their PRI payments towards their annual mandatory payout minimum. That emphasis also justifies not considering such payments as taxable expenditures and excepting them from requirements about prudent investing and caps on levels of equity or profits interests held in for-profit enterprises. Rules regarding self-dealing and co-investing still apply, however.

The main point for purposes of this article is the emphasis on prioritizing charitability under 501(c)(3) along with potential for return of and growth on funds provided as PRIs. For practical guidance on how to implement PRIs, please see our related PRI overview.

Why should foundations make PRIs, especially using equity?

Often grants are ideal for private foundations to pursue their charitable objectives and fulfill their responsibilities. Investing through the endowment facilitates preserving and growing its financial assets and might have some usefulness for pursuing charitable purposes and/or broader concepts of social good. Sometimes, however, the right tool is neither grant nor pure investment because the incentives and opportunities inherent in those tools are not quite right.

Sometimes there are opportunities to focus attention and dollars on solutions and outcomes that align charitability with market participation. Examples might include proving concepts around clean energy, biomedical devices, health care diagnostics and treatments, environmental remediation, tools for education, access to capital by the underserved, or economic development of economically disadvantaged areas and populations, among others.

A foundation might use PRIs because there is potential for money to be returned to and redeployed by the foundation. And why shouldn’t the foundation occasionally be the one to determine how those funds are used – especially to again further its charitable purposes? Moreover, the foundation can participate in economic upsides, which incidentally also can help protect against impermissible private benefit.

A PRI can align incentives of the recipient with the foundation’s charitable purposes, at least to some degree. It can also adapt incentives within the recipient because, unlike grant dollars that are not returned and for which there is no expectation of return, there are different notions of responsibility and accountability. Depending on how the PRI is structured, these incentives might facilitate or inhibit risk taking and resource allocations by the recipient.

Loans, especially if secured in some way, might tend to inhibit responsible risk taking. Guarantees might facilitate responsible risk taking by the recipient while also more directly encouraging others’ commitments and enabling mutual leveraging.

Equity also might facilitate risk taking by the recipient because repercussions of failure can differ from loans. Given charitable pursuits and purposes, a private foundation might want those risks taken. Equity also can provide the foundation with a different type of oversight of management and ability to ensure accountability to its charitable objectives. As an equity holder, a foundation can have more of a voice in decisions about allocation of resources, including towards responsible risk taking and assessing progress towards charitable objectives. A foundation with equity has an opportunity to influence other owners, sometimes even as vocal support for management’s shared priorities. Such a foundation also has a seat at the table when subsequent capital injections into and outflows from the company are being evaluated, including especially their dilution or facilitation of charitable pursuits and results.

Of course, the foundation should ensure that it is knowledgeable, responsible, and careful to not unduly burden the entrepreneurs and managers it is supporting or to protect against inadvertently interfering with its charitable pursuits thereby cutting off its nose to spite its face!

So, why should others use PRIs, especially with equity?

The same considerations about using equity discussed in the preceding paragraphs about foundations apply to charitable and non-charitable investors as well.

Even though they do not have the same compliance obligations as private foundations, charities, endowments, and donor advised funds and their hosts, still must pursue charitable purposes and protect against impermissible private benefit. Using PRI approaches can facilitate both of those requirements. There is a certain discipline inherent in PRIs that these organizations can use to their advantage when appropriate, including channeling strategic thinking and direction while evaluating and forming relationships, setting frameworks for due diligence, negotiating expectations, and establishing parameters for reporting and accountability, among other things.

Of course, family offices, “impact” investors, and other non-charitable investors do not have the same legal responsibilities as private foundations and other 501(c)(3) organizations. But they nonetheless sometimes want to accomplish objectives that align with charitability. They sometimes realize that certain societal gaps and opportunities justify taking a different level of risk to address them. They sometimes want to align incentives (including economic) and direct/leverage resources towards those gaps and opportunities for which there may be financial upsides along with intended charitable results. The PRI’s emphasis on charitability can facilitate these objectives.

Additionally, Foundations can play a crucial catalytic role by structuring PRIs in for profit ventures as opposed to providing grants to charitable institutions. In for profit ventures, non-charitable investors who do not have the same legal responsibilities of foundations, may benefit from the catalytic role of the capital provided by foundations, whereas a grant to a charitable entity would not promote follow on investments by non-charitable investors.

Such non-charitable investors might adapt PRI mechanisms and mindsets to pursue social goods that, while not narrowly charitable, are not necessarily mostly profit-oriented either.

Why others benefit from at least a basic understanding of PRIs, especially equity?

One reason for others to understand PRIs is, as noted in the prior section, because the PRI mechanics and mindset can be adapted to other pursuits and purposes. Another reason is that hopefully more foundations will expand usage of PRIs as part of their toolkit for pursuing their charitable purposes. As that happens, especially if equity approaches are embraced, the likelihood is that other investors’ efforts will overlap with those of foundations – as each leverages the other. Because private foundation compliance with PRI requirements is not optional there is a third reason for others to better understand PRIs. Transactions that involve both foundations and others will become more efficient and less costly. Because no one really wants focus to be on the transactions themselves, understanding will permit quicker and better focus of attention and resources on their respective underlying objectives.