This template agreement is provided to you to facilitate due diligence sharing in impact investment.

ImpactTerms has observed that the investment ticket sizes tend to be smaller in impact investing, compared to traditional investments, resulting in the due diligence costs being disproportionately high. As a result, some impact investments may not be pursued due to these high transactional costs. To combat this, many investors are interested in collaborating on due diligence by sharing their due diligence reports, summaries, and due diligence questions.

This can, however, be hampered by the legal risk of being sued by the recipient of the shared due diligence report if the investment subsequently fails.

In light of the above, ImpactTerms has worked with a major international law firm to draft a template agreement to support due diligence sharing for impact investors.

The agreement includes a limitation on the liability of investors that share due diligence material with third party investors, clarification that this sharing of due diligence material does not constitute investment advice and a limitation on any further distribution of the due diligence material.

This template agreement is intended to be used for US investors. This may be used as the basis for an agreement with investors in other relevant jurisdictions, namely the UK and the European Union.

The Capital Access Lab (CAL) is a national pilot initiative that aims to find, promote, and scale innovative investment managers who are providing new kinds of capital to underserved entrepreneurs and communities in the United States.

In July 2020, the Capital Access Lab announced its investments in 5 funds investing in underserved entrepreneurs through innovative investment structures: 1863 Ventures, Anzu Partners, Capacity Capital, Collab Capital, and Indie.vc. During the selection process of these 5 funds, the Capital Access Lab identified over 100 funds focused on underserved entrepreneurs. This report analyzes the approach of a subset of 20 funds that responded to our survey.

Through our analysis, we learned that funds investing in underserved entrepreneurs through alternative investment structures are often nimble investment vehicles that operate in the very early stages of the portfolio companies’ development, really enabling these companies to raise the first essential capital to fuel their growth. They do not invest exclusively in high growth sectors like traditional VCs; our study shows that they are often sector agnostic and have a wide range of return expectations and initial criteria for the investment that are much more flexible than what we typically see in traditional venture capital.

Whereas these funds face challenges related to covering the structural and operational costs of running an investment fund with relatively low Asset Under Management, they represent a nascent and very targeted approach to serving underserved entrepreneurs. Through this report, we hope to highlight their work, support their growth, and inspire potential funders and donors to invest in them.

BACKGROUND

The Toniic Institute, through the Impact Terms Platform, developed this report about the work of the Ewing Marion Kauffman Foundation and the Capital Access Lab on investment funds adopting alternative investment instruments. The Capital Access Lab is designed to provide risk capital to new investment models that do not resemble traditional venture capital or lending, spurring the formation of new financing mechanisms that increase capital investment to underserved entrepreneurs who have been historically left behind due to their race, ethnicity, gender, socioeconomic class, and/or geographic location.

The objective of this report is to review the lessons learned from the Capital Access Lab’s work and to share innovative ways investors can invest in entrepreneurs who are underserved by venture capital and traditional lending structures. Our goal is to describe emerging approaches to investments, liquidity, and risk/return profiles that can be more inclusive for entrepreneurs.

The Capital Access Lab (CAL), formed in 2019, is a national pilot initiative that aims to find, promote, and scale innovative investment managers who are providing new kinds of capital to underserved entrepreneurs and communities in the United States. The Capital Access Lab was created to help address this capital gap by creating a new vehicle to invest in alternative capital funds survive those entrepreneurs That same year, the Lab’s lead investor and sponsor, the Kauffman Foundation, released a report, titled “Access to Capital for Entrepreneurs: Removing Barriers”, which observed that a surprisingly high percentage of entrepreneurs – more than 83% – do not access bank loans or venture capital.

To source prospective funds, the Capital Access Lab created an online application process through which funds or proposed funds could apply for consideration for funding. The CAL did not widely publicize the announcement of this opportunity and instead relied primarily on word of mouth and limited media. When the fund application was announced, responses far exceeded their expectation. CAL had expected 20 to 40 funds to apply in the first year but ended up receiving close to 150 applications. Of those, over 100 fit the requirements for application. “One of the most positive signals to us – [was that] the submissions were mostly first-time fund managers and aspiring investors wanting to bring capital to their community” said John Tyler, Kauffman Foundation General Counsel. The CAL team was also encouraged and surprised by the diversity of the applicants. Roughly 55% of applicants were women and 50% persons of color. The large and diverse application pool reveals a significant demand for and interest in alternative capital structures.

The CAL had expected that many of the applicants would be larger funds that saw alternative capital structures as an additional opportunity. (Traditionally it is difficult for funds smaller than $10 million in assets to generate enough fees to cover their overhead.) Unexpectedly, the applicant pool included many smaller funds that would have traditionally been considered too small to rely only on traditional management fees, but instead many funds were a part of related organizations that could support the overhead. These related organizations included nonprofit business accelerators, Community Development Financial Institutions (CDFIs), and other organizations that wanted to bring investment capital to their communities. For example, 1863 Ventures, one of the funds that received investment, already had an active business development program and wanted to start an investment fund as a means of furthering its mission.

During their due diligence process, the Capital Access Lab identified over 100 funds focused on underserved entrepreneurs, eventually selecting five: 1863 Ventures, Anzu Partners, Capacity Capital, Collab Capital, and Indie.vc.

The Capital Access Lab includes as one of its initiatives, the Capital Access Lab Fund which is a donor advised fund housed at Impact Assets. That fund was capitalized by the Kaufman Foundation. The Capital Access Lab Fund, and a separate funding source from Rockefeller foundation, have invested in the five funds that were selected by The Capital Access Lab.

To ensure the preservation of a recognized charitable purpose under Section 501(c)(3), the Kauffman Foundation developed a charitability term sheet which it has made publicly available as an example of how a foundation structured a particular investment to further its charitable mission and ensure accountability thereto.

Although CAL could not invest in all the funds, they recognized there was a lot to learn and share about their innovative investment structures. This report analyses the approach of a subset of 20 funds who responded to our survey.

RESEARCH – RESULTS AND ANALYSIS

Toniic and the Impact Terms Platform conducted research for this study using a combination of interviews with the principals and a formal survey. The survey participants consist of funds that had applied to the Capital Access Lab during their initial funding period. Twenty funds participated in the survey. The data below highlights some key takeaways from our review.

FUND CHARACTERISTICS

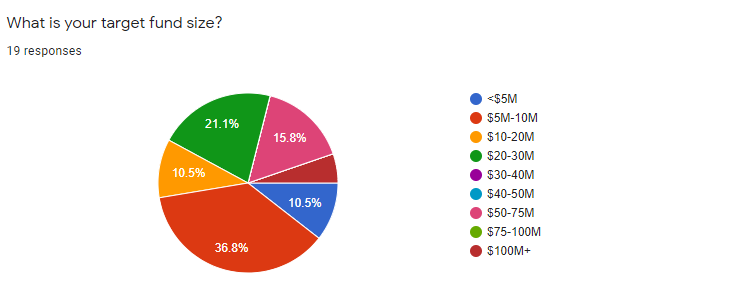

TARGET FUND SIZE

Fifty percent of survey respondents reported a target fund size of less than $10 million.

This target size is consistent with the population of over 100 applicants who applied for funding from CAL – as 50% of those applicants also reported a target size under $10 million. If these funds were to use the traditional VC fee structure that means that they would expect to receive under $200,000 per year in management fees to cover management costs. These low fees are generally considered below the viable amount required by a fund management team without external middle and back office support.

INVESTMENT STAGE

Ninety five percent of participants report that they will invest in seed or pre-seed stage companies. Of those participants, 55% said they would also invest in Series A investments, leaving 45% who only target seed or pre seed stage investing. Only one fund participant would not invest in seed or pre seed stage companies targeting only post seed investments.

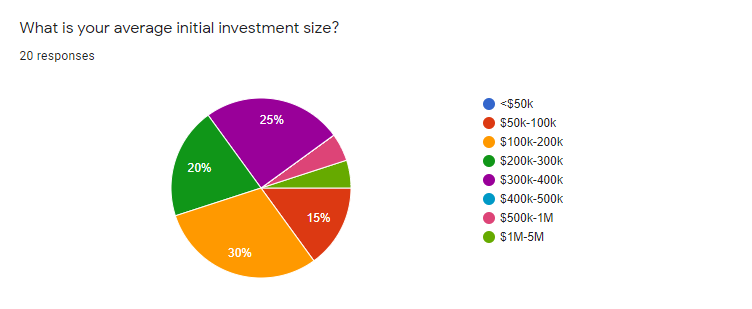

TARGET INVESTMENT SIZE

Consistent with the small average target fund size and largely seed stage investing, 65% of the participants expect to invest less than $300,000 per investment. Only 10% of respondents would invest more than $500,000.

TARGET SECTORS

45% of the respondents have indicated that they are sector agnostic, and 25% of the respondents (among the open-ended responses) included Food and Agriculture as one of their funds’ focus areas.

While traditional VC funds often target high growth sectors such as IT, Health Care, Financials, Telecommunication, the survey respondents did not indicate a strong tendency towards these sectors.

FINANCIAL INSTRUMENTS USED

The following section analyses the financial instruments used by these funds to invest in underserved entrepreneurs. The classification process of these alternative investment structures is a challenging process because there is not an agreed-upon vocabulary for many of the emerging investment structures, nor agreement about whether they should be broadly classified as equity or debt. For example, respondents may have differing opinions about if the Demand Dividend Structure should be debt or equity, so we asked about that structure as both debt and equity then combined them when appropriate to our analysis.

COMMON FEATURES OF ALTERNATIVE INVESTMENT STRUCTURES BASED ON CONTINGENT PAYMENTS

To structure these investments, investors typically start with a target IRR, make a range of estimates of the company’s future performance, and then structure the other terms and features of the investments, including the repayment terms such as the percent of revenues and return multiple cap to achieve that target IRR.

The survey asked a series of questions about the details of the alternative investing structures used by that participant. The questions were designed to get further details around what we anticipated would be the most common structures used: a variation of contingent payment structures. Seventy-five percent of the respondents reported using some form of alternative investment structure based on contingent payments (revenue-based debt, redeemable equity, or Demand Dividends).

These structures are flexible and can be designed to include a variety of features. The core feature of these structures is that they are contingent on something like the amount and timing of the portfolio companies’ revenues. Therefore, the return to the investor will vary based on the features of the investment and the financial performance of the company.

Basis of calculation

Of the 75% participants that stated they will or do use a form of contingent payment structure – 40% said they would invest using gross cash receipts as a basis of calculation, and 47% reported they would invest using net cash receipts. Thirteen percent reported they would use either gross or net cash receipts. Demand Dividend structures did not seem to affect this ratio, even though Demand Dividends typically use net cash receipts as a basis of calculation.

Return Expectations

Respondents reported a wide range of target IRR for their investments ranging from 2% to 35% and averaging 15%. We did not specify if we were asking for the target IRR for the fund or individual investment, but we believe that most participants were answering at the fund level.

Minimum annual revenue required for investment

Respondents reported a wide range of minimum required revenues for the investees ranging from under $50,000 per year to over $5 million per year. The median required revenues was $300,000-$400,000 per year.

Minimum annual revenue growth rate

Respondents reported a median required forecast annual revenue growth of 20-30% with only 16% requiring revenue growth of more than 40%. This differs significantly from the kind of minimum revenue growth requirements you would see from traditional VC.

Half of those who are making revenue based (or similar) finance structures are investing in seed or pre-seed, and will invest into forecast revenue growth below 30%. These characteristics are not common in traditional venture capital so this demonstrates the growth of new sources of capital, that are willing to invest with non-traditional approaches.

Minimum gross margin of target companies

Considering the role that revenues play in the calculation of repayment, we also asked about the minimum required gross margin in order to repay the investment. Respondents reported a minimum median target gross margin of 30-40%. At Impact Terms, our expectation was that lower reported minimum revenue growth rate targets would result in higher the margin requirements. We had this expectation because for an investor to receive a target return of X% on an investment in a lower growth company, that company typically must be able to support a higher percentage of cash flow paid to the investor which requires higher gross margins.

The opposite was the case, as it turned out. The funds that were willing to take the lowest forecast revenue growth in seed stage companies were also willing to take the lowest gross margins. Like the wide range in target IRR, this demonstrates that there is a much wider range of return expectations and minimum requirements than we see in traditional venture capital. One possible explanation is that the funds accepting lower gross margins for lower revenue growth companies are doing so as part of a strategy to provide the appropriate capital to the entrepreneurs. That is, the entrepreneurs they are targeting may simply not have higher revenue growth and margins so the funds used alternative investment structures with return features that the companies could afford.

Percentage of revenue used to repay the investment

Thirty-three percent of respondents indicated that their average percentage of revenues used to repay the investment is 5%, and overall 66.6% indicated an average percentage of revenues lower than 10%. This is typically repaid by the portfolio companies monthly or quarterly out of minimum targeted gross margins of 30-40%.

Average return multiple cap

Thirteen participants use an average return cap – meaning the average cash-on-cash multiple of the invested capital to be returned to the investor over the life of the investment. The industry average return cap is generally between 2x and 3x the initial invested amount. As an example – a cap of 3x on a $100,000 investment would mean the investment is complete when a total of $300,000 has been repaid. This is a common structuring feature of alternative investments that are based on revenue, cash flows or similar contingent payments. The total IRR of that investment would depend on the time it takes for repayment as well as the cap, so a 3x cap investment that takes 10 years to pay out would have a lower IRR than a 3x cap investment that takes 5 years to pay out.

REVIEW AND CONCLUSIONS

It is clear both from the large number of applicants for Capital Access Lab funding and from the follow up research we conducted that there is a significant and underserved ecosystem of small funds that are leveraging alternative investment structures to invest in companies focused on underserved populations. Many of the funds are sector agnostic and not many are targeting traditional venture sectors like IT, Health Care, Financials, Telecommunications. It is also evident from the wide range of return expectations and the combination of investment structuring features that the funds are willing to invest beyond what we would expect from traditional VCs and that therefore that the funds in the survey can serve entrepreneurs who fall outside of traditional VC requirements.

These funds are nimble investment vehicles that operate in the very early stages, potentially being the first professional investors supporting companies in their infancy, effectively de-risking and capitalizing early-stage entrepreneurs.

They also have a wide range of return expectations, including repayment multiples, and initial criteria for the investment that are much more flexible than what we typically see in traditional venture capital. It has long been a complaint that sources of capital are too fixated on structures designed only for companies with explosive growth, so it is encouraging that this research shows an emergence of new capital providers exploring alternatives to traditional expectations and structures.

Out of the 100 funds that applied to the Capital Access Lab, and more specifically out of the 20 survey respondents, we have observed that about 50% of the funds have a target raise of less than $10 million and 75% of less than $30 million; that 95% invest in seed stage, and about ~50% in pre-seed and Series A; and that 65% target an initial investment of less than $300,000 per investment.

Toniic, the global action community for impact investing, has also identified the emergence of relatively small and nimble funds (less than 15M in target AUM) leveraging alternative investment structures to address the needs of underserved populations across different investment themes. These includes funds providing loans to farmers to be repaid through a revenue share agreement in order to allow time to the farmers to switch to organic and regenerative agriculture practices and align their cash flows from higher quality produce with the loan repayment, funds providing capital to minority owned businesses in geographies out of the radar of major venture capitalists to facilitate exits, but also funds providing loans to underserved students that can repay their loans only when they start generating income from actual employment.

While this did not apply to the five funds selected for investment by the Capital Access Lab, these smaller funds are much smaller than typical venture capital fund and CDFI, so small in fact that many are unlikely to cover their operating costs as a fund, and instead use the fund as an addition to existing community service programs. These funds primarily target seed stage companies and are using a wide range of alternative investment structures.

In order to support these experimental but smaller funds, it is clearly important to find ways to lower their operating costs. As noted in this review, important costs like legal, including the added costs associated with using new investing and organization structures, insurance and fund administration are high for these funds. It can even be difficult to find fund administration services that will support alternative investment structures. Companies like AngelList are starting to provide some of these services at lower cost but they are still expensive for small funds and they do not offer services to most alternative investment structures. Investors and foundations who wish to support these funds might consider funding start-ups that help provide these services at lower cost to smaller funds.

Agnes Dasewicz, Lead, Capital Access Lab observed that, alternatively, it would be worth evaluating if investments coming from foundations could, when legally allowed, be accompanied by separate resources and donations to cover some administrative expenses and technical assistance. This is fairly common practice with large international funds who often have sidecar vehicles for technical assistance, and we agree that sidecar grants would help further the ability of small funds to continue to innovate.

More and more wealthy families are interested in using their family assets, their private family foundations, and their donor-advised funds to do more than traditional grant making. They are looking instead to make loans to charities, and loans to‑‑and even equity investments in‑‑for-profit entities that are furthering charitable purposes. By adopting the program-related investments (“PRIs”) approach, a foundation and other investors have an opportunity to recycle the funds as they are repaid, for additional charitable purposes, thereby potentially increasing the long-term impact of their charitable assets.

This article provides information about the mechanics of PRIs, especially from a compliance context for foundations. Even so, there is much that can be adapted from PRIs that can be useful to other investors wanting to advance charitable purposes and outcomes while also preserving, even growing, and eventually recycling their investment.

Who is the PRI investor?

From an IRS compliance standpoint, we generally are talking about private foundations – that is, nonprofit corporations (or trusts) that are tax-exempt under Section 501(c)(3) of the Internal Revenue Code (the “Code”) and that are classified under Section 509(a) as private foundations. To be clear, though, Section 501(c)(3) public charities, including their donor-advised funds, could also take advantage of these investments, as can others.

What is a PRI? What are its advantages for a foundation?

A PRI is an investment that a foundation makes from its charitable pool of assets, not from the assets it intends to invest for purposes of growing the endowment. Therefore, a PRI is not subject to traditional investment policies and prudent investor standards. Nor is a foundation required to limit its levels of ownership as required by the “excess business holdings” rules, although they still must comply with the self-dealing and co-investment rules.

A PRI counts towards satisfying a foundation’s required five percent minimum distribution requirement. Unlike a grant that a foundation does not expect to see any money from, a foundation must understand how to treat money returned to it pursuant to a PRI. That money is of two types: (1) return of the principal or invested amount; and (2) distributions or payments of interest, dividends, or appreciation over and above the first category. Category one returns increase the annual payout obligation of the foundation for the given time period such that the foundation must payout at least 5% for that period plus amounts returned as category one payments. Category two payments are treated as investment income to the foundation, just like any other investment income. Losses — that is returns and payments that do not equal the category one principal or invested amount — are not available to reduce endowment or gains from unrelated business taxable income on which taxes must be paid.

A PRI must satisfy all three of the following tests:

The investment must further one or more charitable purposes of the foundation such that “but for” the investment’s connections to the foundation’s charitable purpose it would not be made. This is a determination specific to each foundation, its mission, and the proposed PRI;

The production of income or the appreciation of property may not be a significant purpose of the investment; and

As is true of any foundation grant, the PRI cannot be used to fund electioneering or lobbying activities.

In addition, when the investment is made in a for-profit entity, the foundation must exercise “expenditure responsibility” over the investment, which involves careful due diligence before making the investment, correct provisions in the investment documents, reporting back to the foundation on the use of funds, proper reporting on the tax return, and follow-up with the investee if it is not properly spending the invested funds.

For additional information on expenditure responsibility, please see the following publications by Adler & Colvin:

Certainly, as the preceding makes clear, foundations have regulatory reasons for complying with these requirements. Other 501(c)(3) organizations can also benefit from adopting these requirements as aids in fulfilling their own legal obligations to ensure charitable use of their assets and to protect against impermissible private benefit. For other than 501(c)(3) investors, adaptations of the above approach can contribute to their objectives, especially approaches to due diligence, reporting, and accountability.

How does a PRI satisfy the charitability requirement?

First, the investment must be intended to further a recognized charitable purpose under Section 501(c)(3). Note that the activity being funded does not have to qualify under Section 501(c)(3). Classic PRI examples include funding a for-profit bank or grocery store in a poor or deteriorating neighborhood that does not have access to these services. Running a grocery store or bank is not charitable, but relieving poverty, giving underserved people easier access to healthy food, combatting community deterioration, and helping communities without access to safe banking, are charitable purposes.

Second, the purpose must be one that is within the foundation’s mission. A foundation whose purposes are limited to supporting public television would not want to make a PRI to put a grocery store in an underserved community.

The Kauffman Foundation has developed a charitability term sheet as an example of how a foundation structured a particular investment to further its charitable mission and ensure accountability thereto. The example involves investing in a private equity fund(s) targeting activities to provide capital to under-represented and underserved entrepreneurs. That is, those who are of color or are women unable to attract capital from traditional sources because of those characteristics and to entrepreneurs whose companies operate in economically disadvantaged areas.

How does a foundation demonstrate that no significant purpose of the investment is profit-oriented?

There is no requirement that the investment fail or that it does not generate a profit – potentially even at market. The test, rather, is one of intent or purpose. Is this the type of investment that the foundation would make under its own investment policy and investment standards? Will other market participants likely participate on the same terms and conditions? If so, then it is not likely going to satisfy the ‘no significant purpose’ test. Some of the factors that foundations should consider in favor of satisfying this test include:

For PRI Loans and Guarantees:

a lower than market interest rate;

no security or weak security;

subordinate positioning relative to others;

banks and other commercial lenders are not willing to loan on these terms; or

the loan is needed as a catalyst for equity investors.

For PRI Equity Investments:

insufficient commercial investors are willing to invest generally or on these terms;

high risk investment, with limited liquidity or risky exit; and

the investment is needed as a catalyst for obtaining loans or other investments.

Complying with this second prong of the PRI elements must be balanced with protecting against others unduly benefiting from the foundation’s positioning. Impermissible private benefits must still be avoided.

Authored by:

Robert A. Wexler; Principal; Adler & Colvin

John E. Tyler III; General Counsel, Secretary, and Chief Ethics Officer; Ewing Marion Kauffman Foundation

Pay For Success is a public-private partnership in which a non-government funder pays the up-front costs for a social service intervention and is repaid by a government actor based on the achievement of previously agreed-upon target outcomes.

The term “pay for success” (“PFS” in shorthand) is most commonly used in the United States. The concept originated in the United Kingdom under the name “social impact bond.” When the concept was introduced in the United States, the name “pay for success” was adopted because not all projects are formulated with a traditional bond structure. In emerging markets, the term “development impact bond” has emerged to describe this concept in an international development context.

CHARACTERISTICS

The principle characteristics of a Pay For Success project are as follows:

A focus on outcomes, rather than outputs. Payments are made based on the outcomes experienced by the people served by the social service intervention, rather than the number of people served. This is a structural shift from how most social services are funded.

Up-front funding by a non-government funder: The social service intervention is paid for by a private investor, philanthropy, or other non-government funder, who can expect to be repaid only if target outcomes are achieved. If the project is unsuccessful — and the target outcomes are not achieved — then that non-government funder is not repaid for the investment. Therefore, taxpayers are not responsible for paying for an intervention that did not work as planned.

HISTORY

The concept was originated by Sir Ronald Cohen in the UK.

The first social impact bond was implemented at Peterborough Prison near York, UK. In that project, a private investor paid for people who were preparing to be released from prison but deemed to be at a higher risk for re-offending to participate in a new recidivism diversion program. The UK government agreed to repay the investor if recidivism among the participants was reduced by a targeted percentage. The project launched in 2010 and concluded in 2015, with findings that showed a reduction in reoffending. Results: https://www.rand.org/randeurope/research/projects/social-impact-bonds.html

In 2010, the US federal government under President Barack Obama began adapting the concept for use by state and local grantees of federal funding from the US Departments of Labor, Education, and Justice. This work was centralized under the White House Domestic Policy Council’s Office of Social Innovation and Civic Participation. The first projects in the US launched in 2012.

ACTORS IN PAY FOR SUCCESS

Each pay for success project or initiative has the following actors participating:

Government actor: A government agency is responsible for paying for outcomes upon achievement, based on terms agreed upon by all parties in the project negotiation. Repayment is generally expected to be consistent with the money the government is saving due to the intervention. For example, a reduction in the number of formerly incarcerated people reoffending leads, in theory, to fewer prisoners that the government must support.

Service provider: The social service intervention is provided by a non-profit or for-profit organization. The service provider contracts with the non-government actor making the up-front investment, so they are paid for delivering the intervention regardless of impact. Typically, the service provider is selected by the investor, with review or approval from the government, through a competitive process and must demonstrate expertise or a track record of success in delivering the service to the target population.

Non-government funder: A non-government funder pays the upfront costs of the service provider to deliver the social service intervention to the target population. This non-government actor is often a private investor, but could also be a philanthropy, community foundation, high net worth individual, or other funder. If the social service intervention reaches agreed-upon outcomes, the actor is repaid. If not, the actor is expected to take the loss.

Evaluator: An independent evaluator is contracted to perform an independent evaluation of the social service intervention provided to the target population, to determine whether agreed-upon outcomes were met. The rigor of the evaluation, including the use of a control group, is determined by the parties involved.

Intermediary organization: Most PFS projects have an intermediary organization that serves a mediation and management role. This organization brings the parties together to create the project and agree on the target outcomes to be achieved. The work of the intermediary organization is often funded by philanthropic donations.

Concern that PFS would siphon money from existing social programs and/or private them has not come to fruition. Model is intended to validate/test whether a new service/intervention is more effective then status quo — governments may or may not end up using that information

Evaluations: An independent evaluation is a core part of a pay for success project. The expectations for the rigor of that evaluation have been debated, particularly in the wake of Urban Institute and other early field leaders have argued that PFS project evaluations should be randomized control trials (RCTs) unless there is a compelling reason to use a less rigorous method.

Scalability: Since the launch of the first pay for success projects, a major critique of the model has been the cost of putting projects together. Philanthropic grants are generally still required to fund the 18-to-24-month process.

Concern that governments will not scale successful projects – too early to tell

Capacity building for nonprofits

Case Studies

In 2015, India pioneered the world’s first development impact bond (DIB) where the outcome payer was a private foundation. Read more in the following case study from AVPN:

Collective Investment Vehicles aggregate capital from multiple investors into a single investment entity. Generally, the purpose of Collective Investment Vehicles is to invest in a portfolio of companies or projects, although, in some instances, special purpose vehicles are created for a single investment whose capital requirements exceed the available capital that a single investor is willing to commit.

Collective Investment Vehicles are managed by professional investment managers in order to leverage their professional experience, full time dedication, and comprehensive risk management practices.

The aggregation of capital in a single vehicle also improves economies of scale by spreading transaction costs (such as due diligence costs) over a larger pool of capital, as well as the risk return profile by diversifying the assets of the vehicle through a portfolio of investments.

Fund Managers’ view

Collective Investment Vehicles are managed by professional asset managers, who are the agents of the firm. The managers take investment decisions on behalf of the collective investment vehicle, and are remunerated for the management of the vehicle as well as for the performance of the investments.

In the impact investing industry, impact fund managers often have relevant industry investment and thematic experience, ability to operate in frontier or undercapitalized markets, and relevant professional networks which they can make available to investors in an investment vehicle.

Among the most important factors for managers are that the Collective Investment Vehicle be adequately capitalized and that the managers have the time and flexibility to execute their investment strategy.

Investors’ view

For the investors in the Collective Investment Vehicles, it is important that the investment thesis implemented by the manager delivers the expected financial returns and social and environmental impact, while maintaining adequate risk mitigation practices.

The benefits of pooling capital into a single Collective Investment Vehicle include:

Having access to a portfolio of investments

Diversification

Professional management team dedicated to managing investments

Traditional impact fund structure

Limited Partnership Closed Ended Fund

The most common structure for Collective Investment Vehicles in venture and private equity is the limited partnership. This structure separates the fund managers, the General Partners (GPs), who manage the fund and take investment decisions. The GPs bear unlimited liability for the obligations of the fund. They raise capital from investors in the fund known as Limited Partners (LPs), who are not involved in the investment decisions and have limited liability (for the amount the invested in the fund?). The limited partnership is a closed ended fund with a fixed life, and standard provisions that regulate the distribution of capital to protect the invested capital of Limited Partners before capital distributions are made to the General Partners.

“A Limited Partnership Agreement regulates the relationship between the General Partners and the Limited Partners, covering terms, fees, investment structures, and other items that require mutual agreement before investment.

Carried interest, also known as “carry” or “profit participation,” is the share in the profits generated through the investments that the general partner receives from the fund. The terms of the Carried Interest vary, and may or may not be payable to the GP only after achieving a Hurdle Rate.

Management fee

The management fee is the fee charged by the General Partner to the fund for running the day-to-day operation of the fund, and is paid from the paid in capital annually.

Alternative Structures

Even though Limited Partnerships are the most common vehicle to structure funds in impact investing (GIIN), alternative terms or collective investment vehicles structures have emerged In impact investing to overcome intrinsic features of the Limited Partnership model.

Alternative performance incentives

In a conventional limited partnership, the Limited Partners handle all the investment decisions and management of the investment portfolio over to the General Partners. As a result of this delegation, the Limited Partners have no control over the impact management of the portfolio investment.

In order to better align the financial incentives of the General Partners to the impact expectations of the Limited Partners, innovative structures to align the financial remuneration of the General Partners to the impact results have emerged.

The Carried Interest is the profit participation of the General Partner in the fund, which is calculated on the returns of the fund that exceed the invested capital. The Carried Interest can be tiered or unlocked based on the achievement of specific social impact metrics.

Holding Company Structures

Holding Companies (HoldCos, or permanent capital vehicles, or evergreen investment structures) are deployed to extend the lifetime of an investment vehicle beyond the traditional 10 years plus extension of a close ended fund (limited partnership investment fund).

The longer lifetime of the investment vehicle gives additional flexibility to the fund manager in investing patiently in a social enterprise, and does not require exiting the investment within the closed ended lifetime of a traditional limited partnership structure. Patient capital and a longer investment period can facilitate a mission aligned exit of the investment in social enterprises when the company has fewer prospective target buyers and chances of an initial public offering.

Liquidity to investors

Liquidity to investors While limited partnerships must return the invested capital after returns and fees to the investors throughout the lifetime of the limited partnership, typically HoldCos do not have a limited lifetime. In order to provide liquidity to investors, in addition to providing dividends, HoldCos can redeem and buy back existing shares, facilitate secondary liquidity by transferring shares among investors, or list on the stock market to raise additional capital and provide liquidity to existing investors.

Potential for listing on the stock market Holding companies are investment vehicles that can offer secondary liquidity to investors, as well as attract new capital from new investors, through an Initial Public Offering.

Budget

While limited partnerships operate through the yearly management fee calculated on committed or invested capital, holding companies typically are managed on an operating budget. Innovative approaches to determine a cost based fee calculation have emerged, which limit the operational expenses to the actual operational expense and is capped to the invested capital.

Unlike traditional corporate structures, in the US, a benefit corporation obligates the board to consider the interests of all stakeholders in its decision making, not just shareholders. The company must pursue a public benefit purpose, and must report on its impact performance to shareholders and potentially to the general public (depending on the state). The definition of public benefit varies by state, but it is most often expressed as a purpose of creating a positive impact on society and the environment as a whole, or of operating in a responsible and sustainable manner. The statutes also allow (or in some states require) the company to specify one or more specific public benefit purposes that it will pursue, each of which must fall within statutory definitions. For example, Delaware requires the specific public benefit purpose to be stated in the certificate of incorporation, and allows it to include positive effects of “an artistic, charitable, cultural, economic, educational, environmental, literary, medical, religious, scientific or technological nature.”

Some states, including New York, also allow the company to specify which purposes have priority. Practitioners should keep in mind that provisions prioritizing one purpose over others run the risk of limiting the board’s discretion.

Benefit corporations are often conflated with certified B Corporations (or B Lab certifications or B Corp certifications). Benefit corporation is a legal status conferred by state law in the US; whereas B Lab certification is issued by a private organization and has no legislative framework. B Lab certification is not needed to obtain benefit corporation status. Non-profit B Lab, which issues B Corporation Certifications to organizations that commit to a set of impact “best practices”, also advocates for the adoption and improvement of benefit corporation.

Term sheet language specific to benefit corporations may be useful in the following situations:

the corporation will be formed at the time of the investment, and so the specific public benefit has not yet been defined;

the investors want to modify the definition of the specific public benefit in connection with the investment;

the investors or entrepreneurs want to require that the benefit report be distributed more often than is statutorily required;

the investors or entrepreneurs want to require the company to publicly share its benefit report;

the investors or entrepreneurs want to require the enterprise to assess its performance with respect to its specified public benefit against an independent third party standard;

the investors want a voice in any future changes to the benefit purpose and related concepts; and

if the company has multiple specific benefit purposes, the investors or entrepreneurs may want to specify that the company prioritize one or more purposes over others.

With some of the sample language, we identify a state or states for which the language is designed. Adjustments may be required to this language for corporations formed in other states.

Agreeing on a company’s specific public benefit purpose:

Sample language: The [Certificate][Articles] of Incorporation of the Company shall identify as the Company’s specific public benefit purpose(s) [definition of specific public benefit purpose(s)].

Requiring more frequent benefit reporting:

Sample language: The Company shall provide to its shareholders its benefit report [insert time period, which is more frequent than statutorily required].

Requiring public dissemination of benefit reports:

Sample language: The Company’s benefit report shall be posted on the Company’s website. The Company may omit from the posted reports any financial or proprietary information included in the reports.

Requiring assessment of social performance with reference to third party standards:

Sample language: The Company’s benefit report shall include an assessment of the overall social and environmental performance of the Company against a credible, independent third party standard].

Requiring investor approval of specific benefit purpose and related items:

(Sample language – Delaware Debt): During the term of the Loan, the consent of the Investor shall be required to (1) change the Company’s specific public benefit purpose(s), (2) adopt or change the objectives the Board is required to establish to promote its public benefit purpose(s) and the interests of those materially affected by the Company’s conduct, or (3) adopt or change the standards the Board is required to adopt to measure progress in promoting such public benefit purpose(s) and interests.

Sample language (Delaware equity): As long as the Investors hold at least [X percent] of the Shares purchased, [the vote of at least X percent of the Shares, voting as a separate class] OR [the approval of the Board, including the approval of the Series X Director(s)], shall be required to (1) change the Company’s specific public benefit purpose(s), (2) adopt or change the objectives the Board is required to establish to promote its public benefit purpose(s) and the interests of those materially affected by the Company’s conduct, or (3) adopt or change the standards the Board is required to adopt to measure progress in promoting such public benefit purpose(s) and interests.

Sample language – NY/CA debt): During the term of the Loan, the consent of the Investor shall be required to (1) change the Company’s specific public benefit purpose(s), or (2) adopt or change the third-party standard used to assess the Company’s social and environmental performance.

Sample language (NY/CA equity): As long as the Investors hold at least X percent of the Shares purchased, [the vote of at least X percentage of the Shares, voting as a separate class] OR [the approval of the Board, including the approval of the Series X Director(s)], shall be required to (1) change the Company’s specific public benefit purpose(s), or (2) adopt or change the third-party standard used to assess the Company’s social and environmental performance.

Establishing priority of multiple public benefit purposes

Sample language: The [Certificate][Articles] of Incorporation of the Company shall identify as the Company’s specific public benefit purpose(s) [definition of the specific public benefit purpose], and shall state the Company’s intention to give priority to [definition of the priority purpose].