EXECUTIVE SUMMARY

The Capital Access Lab (CAL) is a national pilot initiative that aims to find, promote, and scale innovative investment managers who are providing new kinds of capital to underserved entrepreneurs and communities in the United States.

In July 2020, the Capital Access Lab announced its investments in 5 funds investing in underserved entrepreneurs through innovative investment structures: 1863 Ventures, Anzu Partners, Capacity Capital, Collab Capital, and Indie.vc. During the selection process of these 5 funds, the Capital Access Lab identified over 100 funds focused on underserved entrepreneurs. This report analyzes the approach of a subset of 20 funds that responded to our survey.

Through our analysis, we learned that funds investing in underserved entrepreneurs through alternative investment structures are often nimble investment vehicles that operate in the very early stages of the portfolio companies’ development, really enabling these companies to raise the first essential capital to fuel their growth. They do not invest exclusively in high growth sectors like traditional VCs; our study shows that they are often sector agnostic and have a wide range of return expectations and initial criteria for the investment that are much more flexible than what we typically see in traditional venture capital.

Whereas these funds face challenges related to covering the structural and operational costs of running an investment fund with relatively low Asset Under Management, they represent a nascent and very targeted approach to serving underserved entrepreneurs. Through this report, we hope to highlight their work, support their growth, and inspire potential funders and donors to invest in them.

BACKGROUND

The Toniic Institute, through the Impact Terms Platform, developed this report about the work of the Ewing Marion Kauffman Foundation and the Capital Access Lab on investment funds adopting alternative investment instruments. The Capital Access Lab is designed to provide risk capital to new investment models that do not resemble traditional venture capital or lending, spurring the formation of new financing mechanisms that increase capital investment to underserved entrepreneurs who have been historically left behind due to their race, ethnicity, gender, socioeconomic class, and/or geographic location.

The objective of this report is to review the lessons learned from the Capital Access Lab’s work and to share innovative ways investors can invest in entrepreneurs who are underserved by venture capital and traditional lending structures. Our goal is to describe emerging approaches to investments, liquidity, and risk/return profiles that can be more inclusive for entrepreneurs.

The Capital Access Lab (CAL), formed in 2019, is a national pilot initiative that aims to find, promote, and scale innovative investment managers who are providing new kinds of capital to underserved entrepreneurs and communities in the United States. The Capital Access Lab was created to help address this capital gap by creating a new vehicle to invest in alternative capital funds survive those entrepreneurs That same year, the Lab’s lead investor and sponsor, the Kauffman Foundation, released a report, titled “Access to Capital for Entrepreneurs: Removing Barriers”, which observed that a surprisingly high percentage of entrepreneurs – more than 83% – do not access bank loans or venture capital.

To source prospective funds, the Capital Access Lab created an online application process through which funds or proposed funds could apply for consideration for funding. The CAL did not widely publicize the announcement of this opportunity and instead relied primarily on word of mouth and limited media. When the fund application was announced, responses far exceeded their expectation. CAL had expected 20 to 40 funds to apply in the first year but ended up receiving close to 150 applications. Of those, over 100 fit the requirements for application. “One of the most positive signals to us – [was that] the submissions were mostly first-time fund managers and aspiring investors wanting to bring capital to their community” said John Tyler, Kauffman Foundation General Counsel. The CAL team was also encouraged and surprised by the diversity of the applicants. Roughly 55% of applicants were women and 50% persons of color. The large and diverse application pool reveals a significant demand for and interest in alternative capital structures.

The CAL had expected that many of the applicants would be larger funds that saw alternative capital structures as an additional opportunity. (Traditionally it is difficult for funds smaller than $10 million in assets to generate enough fees to cover their overhead.) Unexpectedly, the applicant pool included many smaller funds that would have traditionally been considered too small to rely only on traditional management fees, but instead many funds were a part of related organizations that could support the overhead. These related organizations included nonprofit business accelerators, Community Development Financial Institutions (CDFIs), and other organizations that wanted to bring investment capital to their communities. For example, 1863 Ventures, one of the funds that received investment, already had an active business development program and wanted to start an investment fund as a means of furthering its mission.

During their due diligence process, the Capital Access Lab identified over 100 funds focused on underserved entrepreneurs, eventually selecting five: 1863 Ventures, Anzu Partners, Capacity Capital, Collab Capital, and Indie.vc.

The Capital Access Lab includes as one of its initiatives, the Capital Access Lab Fund which is a donor advised fund housed at Impact Assets. That fund was capitalized by the Kaufman Foundation. The Capital Access Lab Fund, and a separate funding source from Rockefeller foundation, have invested in the five funds that were selected by The Capital Access Lab.

To ensure the preservation of a recognized charitable purpose under Section 501(c)(3), the Kauffman Foundation developed a charitability term sheet which it has made publicly available as an example of how a foundation structured a particular investment to further its charitable mission and ensure accountability thereto.

Although CAL could not invest in all the funds, they recognized there was a lot to learn and share about their innovative investment structures. This report analyses the approach of a subset of 20 funds who responded to our survey.

RESEARCH – RESULTS AND ANALYSIS

Toniic and the Impact Terms Platform conducted research for this study using a combination of interviews with the principals and a formal survey. The survey participants consist of funds that had applied to the Capital Access Lab during their initial funding period. Twenty funds participated in the survey. The data below highlights some key takeaways from our review.

FUND CHARACTERISTICS

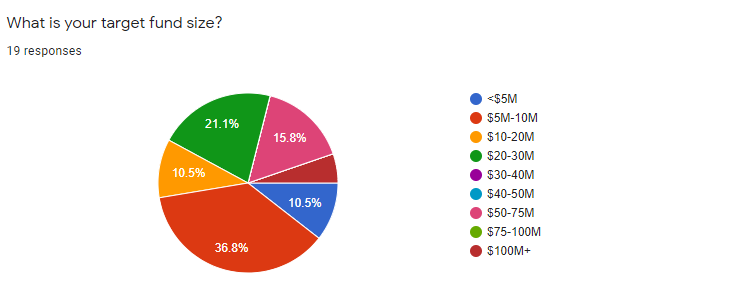

TARGET FUND SIZE

Fifty percent of survey respondents reported a target fund size of less than $10 million.

This target size is consistent with the population of over 100 applicants who applied for funding from CAL – as 50% of those applicants also reported a target size under $10 million. If these funds were to use the traditional VC fee structure that means that they would expect to receive under $200,000 per year in management fees to cover management costs. These low fees are generally considered below the viable amount required by a fund management team without external middle and back office support.

INVESTMENT STAGE

Ninety five percent of participants report that they will invest in seed or pre-seed stage companies. Of those participants, 55% said they would also invest in Series A investments, leaving 45% who only target seed or pre seed stage investing. Only one fund participant would not invest in seed or pre seed stage companies targeting only post seed investments.

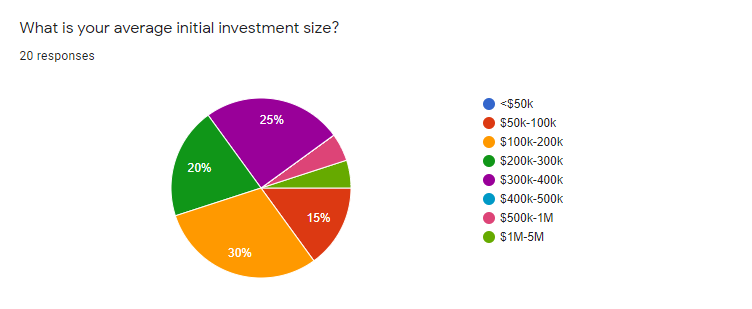

TARGET INVESTMENT SIZE

Consistent with the small average target fund size and largely seed stage investing, 65% of the participants expect to invest less than $300,000 per investment. Only 10% of respondents would invest more than $500,000.

TARGET SECTORS

45% of the respondents have indicated that they are sector agnostic, and 25% of the respondents (among the open-ended responses) included Food and Agriculture as one of their funds’ focus areas.

While traditional VC funds often target high growth sectors such as IT, Health Care, Financials, Telecommunication, the survey respondents did not indicate a strong tendency towards these sectors.

FINANCIAL INSTRUMENTS USED

The following section analyses the financial instruments used by these funds to invest in underserved entrepreneurs. The classification process of these alternative investment structures is a challenging process because there is not an agreed-upon vocabulary for many of the emerging investment structures, nor agreement about whether they should be broadly classified as equity or debt. For example, respondents may have differing opinions about if the Demand Dividend Structure should be debt or equity, so we asked about that structure as both debt and equity then combined them when appropriate to our analysis.

COMMON FEATURES OF ALTERNATIVE INVESTMENT STRUCTURES BASED ON CONTINGENT PAYMENTS

To structure these investments, investors typically start with a target IRR, make a range of estimates of the company’s future performance, and then structure the other terms and features of the investments, including the repayment terms such as the percent of revenues and return multiple cap to achieve that target IRR.

The survey asked a series of questions about the details of the alternative investing structures used by that participant. The questions were designed to get further details around what we anticipated would be the most common structures used: a variation of contingent payment structures. Seventy-five percent of the respondents reported using some form of alternative investment structure based on contingent payments (revenue-based debt, redeemable equity, or Demand Dividends).

These structures are flexible and can be designed to include a variety of features. The core feature of these structures is that they are contingent on something like the amount and timing of the portfolio companies’ revenues. Therefore, the return to the investor will vary based on the features of the investment and the financial performance of the company.

Basis of calculation

Of the 75% participants that stated they will or do use a form of contingent payment structure – 40% said they would invest using gross cash receipts as a basis of calculation, and 47% reported they would invest using net cash receipts. Thirteen percent reported they would use either gross or net cash receipts. Demand Dividend structures did not seem to affect this ratio, even though Demand Dividends typically use net cash receipts as a basis of calculation.

Return Expectations

Respondents reported a wide range of target IRR for their investments ranging from 2% to 35% and averaging 15%. We did not specify if we were asking for the target IRR for the fund or individual investment, but we believe that most participants were answering at the fund level.

Minimum annual revenue required for investment

Respondents reported a wide range of minimum required revenues for the investees ranging from under $50,000 per year to over $5 million per year. The median required revenues was $300,000-$400,000 per year.

Minimum annual revenue growth rate

Respondents reported a median required forecast annual revenue growth of 20-30% with only 16% requiring revenue growth of more than 40%. This differs significantly from the kind of minimum revenue growth requirements you would see from traditional VC.

Half of those who are making revenue based (or similar) finance structures are investing in seed or pre-seed, and will invest into forecast revenue growth below 30%. These characteristics are not common in traditional venture capital so this demonstrates the growth of new sources of capital, that are willing to invest with non-traditional approaches.

Minimum gross margin of target companies

Considering the role that revenues play in the calculation of repayment, we also asked about the minimum required gross margin in order to repay the investment. Respondents reported a minimum median target gross margin of 30-40%. At Impact Terms, our expectation was that lower reported minimum revenue growth rate targets would result in higher the margin requirements. We had this expectation because for an investor to receive a target return of X% on an investment in a lower growth company, that company typically must be able to support a higher percentage of cash flow paid to the investor which requires higher gross margins.

The opposite was the case, as it turned out. The funds that were willing to take the lowest forecast revenue growth in seed stage companies were also willing to take the lowest gross margins. Like the wide range in target IRR, this demonstrates that there is a much wider range of return expectations and minimum requirements than we see in traditional venture capital. One possible explanation is that the funds accepting lower gross margins for lower revenue growth companies are doing so as part of a strategy to provide the appropriate capital to the entrepreneurs. That is, the entrepreneurs they are targeting may simply not have higher revenue growth and margins so the funds used alternative investment structures with return features that the companies could afford.

Percentage of revenue used to repay the investment

Thirty-three percent of respondents indicated that their average percentage of revenues used to repay the investment is 5%, and overall 66.6% indicated an average percentage of revenues lower than 10%. This is typically repaid by the portfolio companies monthly or quarterly out of minimum targeted gross margins of 30-40%.

Average return multiple cap

Thirteen participants use an average return cap – meaning the average cash-on-cash multiple of the invested capital to be returned to the investor over the life of the investment. The industry average return cap is generally between 2x and 3x the initial invested amount. As an example – a cap of 3x on a $100,000 investment would mean the investment is complete when a total of $300,000 has been repaid. This is a common structuring feature of alternative investments that are based on revenue, cash flows or similar contingent payments. The total IRR of that investment would depend on the time it takes for repayment as well as the cap, so a 3x cap investment that takes 10 years to pay out would have a lower IRR than a 3x cap investment that takes 5 years to pay out.

REVIEW AND CONCLUSIONS

It is clear both from the large number of applicants for Capital Access Lab funding and from the follow up research we conducted that there is a significant and underserved ecosystem of small funds that are leveraging alternative investment structures to invest in companies focused on underserved populations. Many of the funds are sector agnostic and not many are targeting traditional venture sectors like IT, Health Care, Financials, Telecommunications. It is also evident from the wide range of return expectations and the combination of investment structuring features that the funds are willing to invest beyond what we would expect from traditional VCs and that therefore that the funds in the survey can serve entrepreneurs who fall outside of traditional VC requirements.

These funds are nimble investment vehicles that operate in the very early stages, potentially being the first professional investors supporting companies in their infancy, effectively de-risking and capitalizing early-stage entrepreneurs.

They also have a wide range of return expectations, including repayment multiples, and initial criteria for the investment that are much more flexible than what we typically see in traditional venture capital. It has long been a complaint that sources of capital are too fixated on structures designed only for companies with explosive growth, so it is encouraging that this research shows an emergence of new capital providers exploring alternatives to traditional expectations and structures.

Out of the 100 funds that applied to the Capital Access Lab, and more specifically out of the 20 survey respondents, we have observed that about 50% of the funds have a target raise of less than $10 million and 75% of less than $30 million; that 95% invest in seed stage, and about ~50% in pre-seed and Series A; and that 65% target an initial investment of less than $300,000 per investment.

Toniic, the global action community for impact investing, has also identified the emergence of relatively small and nimble funds (less than 15M in target AUM) leveraging alternative investment structures to address the needs of underserved populations across different investment themes. These includes funds providing loans to farmers to be repaid through a revenue share agreement in order to allow time to the farmers to switch to organic and regenerative agriculture practices and align their cash flows from higher quality produce with the loan repayment, funds providing capital to minority owned businesses in geographies out of the radar of major venture capitalists to facilitate exits, but also funds providing loans to underserved students that can repay their loans only when they start generating income from actual employment.

While this did not apply to the five funds selected for investment by the Capital Access Lab, these smaller funds are much smaller than typical venture capital fund and CDFI, so small in fact that many are unlikely to cover their operating costs as a fund, and instead use the fund as an addition to existing community service programs. These funds primarily target seed stage companies and are using a wide range of alternative investment structures.

In order to support these experimental but smaller funds, it is clearly important to find ways to lower their operating costs. As noted in this review, important costs like legal, including the added costs associated with using new investing and organization structures, insurance and fund administration are high for these funds. It can even be difficult to find fund administration services that will support alternative investment structures. Companies like AngelList are starting to provide some of these services at lower cost but they are still expensive for small funds and they do not offer services to most alternative investment structures. Investors and foundations who wish to support these funds might consider funding start-ups that help provide these services at lower cost to smaller funds.

Agnes Dasewicz, Lead, Capital Access Lab observed that, alternatively, it would be worth evaluating if investments coming from foundations could, when legally allowed, be accompanied by separate resources and donations to cover some administrative expenses and technical assistance. This is fairly common practice with large international funds who often have sidecar vehicles for technical assistance, and we agree that sidecar grants would help further the ability of small funds to continue to innovate.